Student of the Industry: Is Surplus Lines on a Tear?

By: Paul Buse

Recently I asked myself, “Is surplus lines on a tear?”

Why did I think to ask this?

I was looking at property-casualty industry premium data and I noticed direct written premiums for several insurers had grown dramatically. Well-established insurers with over $500 million in premiums, such as National Fire & Marine, Indian Harbor Insurance Company and James River Insurance Company, showed an increase in premiums of over 25% from 2017 to 2019.

On looking further at insurers that were growing the fastest, I noticed some large premium increases over the same period from insurers I was not familiar with, such as Ategrity Specialty, Blue Hill Specialty and Trisura Specialty Insurance Company.

Then, I noticed the common thread of these rapidly growing insurers: surplus lines.

Standard industry reports and data from the National Association of Insurance Commissioners provide insight on surplus lines, so I did some analysis. The most easily accessible data is based on a full calendar year and, for insurers that write surplus lines from 2015 to 2019, showed favorable growth rates.

Growth rates for surplus lines insurers are an average 8.8%. In contrast, the total p-c market grew at a rate of 4.7%. Perhaps the most interesting element of surplus lines growth is it appears to be accelerating:

- 2015 to 2016: 0.4%

- 2016 to 2017: 5.3%

- 2017 to 2018: 10.3%

- 2018 to 2019: 15.8%

The acceleration of the surplus lines growth rate made me curious about the most current data available: quarterly direct written premiums. What would data through the end of the most recent quarter—ending on Sept. 30, 2020—show?

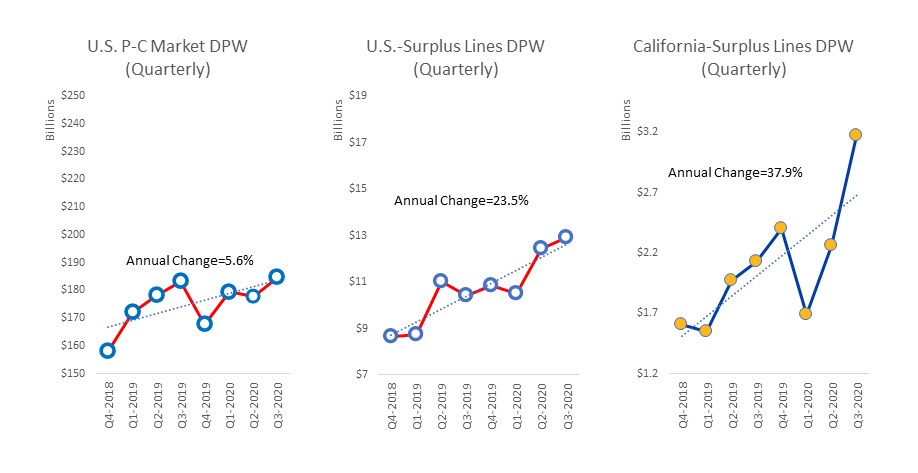

Below is the data for the last two years for all U.S. p-c premiums including surplus lines, surplus lines separated from all premiums, and then surplus lines in the largest premium state: California.

This data was obtained by looking at the quarterly filings of the approximately 2,900 policy-issuing insurers domiciled in the U.S. On a quarterly basis, each insurer must file their direct written premium and their licensed status: “L” (licensed/admitted), “E” (surplus lines-approved), “D” (surplus lines in home state), “R” (risk retention group) or “Q” (reinsurer). Taking premium data for any insurer filing premiums as an “E” or “D” provides the two right-hand charts below.

Source: A.M. Best Company. Used with permission.

Source: A.M. Best Company. Used with permission.

On inspecting this data, I would say surplus lines in California can be defined as “on a tear,” especially if the surge from the second quarter to the third quarter continues. If you noticed the different vertical axis used for direct written premium in the above three graphs, you are an excellent student of the industry! The changing scales are not meant to mislead but to visually display the calculated trends via an approximate slope of the trend line. The slopes are, however, not precisely to scale. Managing the different magnitudes of direct written premium in a side-by-side presentation is a challenge when the total dollars involved vary so greatly on an absolute basis. Focus your attention on the actual percentage increase versus the precise slope of the trend line.

Paul Buse is principal, founder and owner of Real Insurance Solutions Consulting.

This Student of the Industry article is part of a monthly column on IAMagazine.com. Keep an eye on Thursday’s weekly News & Views e-newsletter in February for the next off-beat take on current trends in the insurance industry.

This month’s issue

The May issue is out now!