The Growing Cost of Wildfires: Getting Ready for Forest Fire Season

By: Ben Jones

Since wildfire records began in 1983, there has been a 223% increase in wildfires, according to the National Interagency Fire Center. In 2022 alone, there were 68,988 wildfires in the U.S. compared to 58,985 in 2021, a 16.96% increase. Wildfire seasons are getting longer and more destructive, according to CoreLogic, with the annual destruction of wildfires during the last 10 years at an average of 6.8 million acres, compared to 2.7 million acres between 1983 and 1992. These fires are a growing concern for everyone, and insurance companies are no exception.

2020 was one of the costliest in history, with wildfires causing $16.5 billion in damages. This not only impacts government bodies and utility companies who are responsible for repairing damages to infrastructure, but it also impacts homeowners in high-risk areas. This continues to have an effect on insurance everywhere.

The financial cost is just one half of the story: The health impacts of wildfire exposure are evident in studies linking wildfires to asthma, cardiovascular complications, pulmonary disease and, in some cases, early mortality, according to The Medical Care Blog, sponsored by the American Public Health Association.

While there doesn’t appear to be any immediate impact of increased fires on health insurance, increasing rates of these types of illness may have an effect in years to come.

Data analytics company Verisk Analytics has identified that more than 4.5 million homes in the U.S. are at high risk for wildfires in 2023.

How This Impacts Carriers and Agents

The First Street Foundation Wildfire Model estimates the current risk of wildfire on a property-by-property basis across the country. It also estimates the risk for the next 30 years.

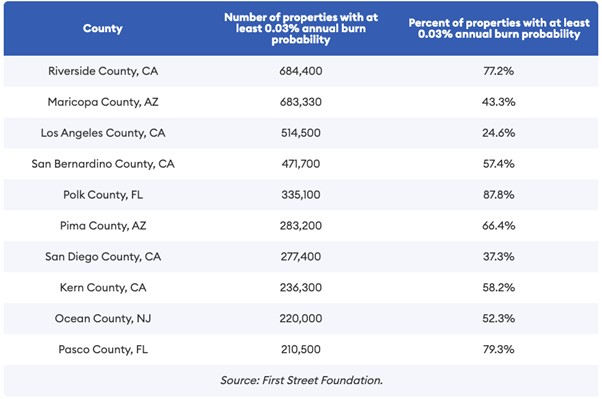

California continues to be one of the most affected states, along with Texas, Arizona, Florida and Oklahoma, according to the model. Insurers covering those parts of the country should start to put measures in place if they haven’t already.

And with supply chain issues causing construction material shortages in the U.S. that are predicted to continue into 2023, according to Mortenson, scarcity is likely to result in increased repair costs, leading to larger claims.

As a result, homeowners are more likely to be shopping for policies that include outside dwellings, such as outhouses, decking and garages, particularly those in rural areas. This is something to consider when putting together their policies.

How Insurance Is Adapting to This New Landscape

An obvious effect of increased wildfires is for insurers to increase their prices with some insurers refusing to insure high-risk properties.

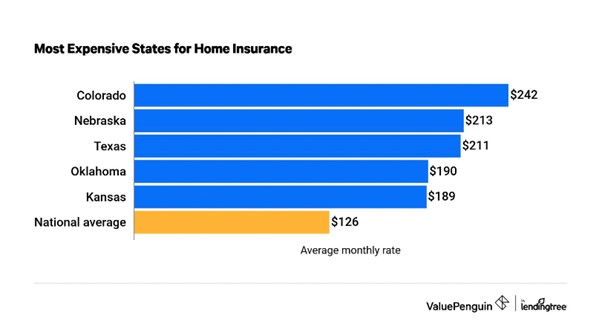

“The states with the highest home insurance costs are generally where natural disasters occur most frequently. Colorado leads the pack, with wildfires pushing prices much higher than the national average,” according to a 2023 article by Value Penguin.

And while this looks set to continue, it seems increasingly likely that insurers will be unable to renew some homeowners.

Further, homeowners who can find cover may wish to add extended or guaranteed cost coverage to their homeowners insurance policies. Another consideration agents should keep in mind is finding insurers with the resources available to focus on risk mitigation and wildfire monitoring through early wildfire detection software, data analysis and closely monitoring wildfire predictions.

So, what does the future look like in high-risk areas?

California has been working on innovative ways to protect communities from overwhelming wildfire costs by creating community insurance in the form of a $21 billion compensation fund to cover some homeowner losses as a result of wildfire. This sort of initiative will lighten the load on insurers and help them to operate as normal.

Wildfire mitigation and data tracking can also help. Some states and organizations have developed real-time map tracking to provide up-to-date information on wildfires, such as NASA’s Fire Information for Resource Management System (FIRMS). Having access to this information can help insurers more accurately predict which properties are at high risk and can influence their underwriting.

Independent agents may choose to partner with consultants on fireproofing homes for customers as an alternative or add-on service. Ultimately, homeowners are looking to experts for advice and this may present an opportunity for agents to bridge that gap.

The costs of wildfires are only going to continue to rise as the climate continues to change. Insurance companies are starting to take note and adapt their policies and rates accordingly. But there is still a long way to go before insurance companies can provide adequate coverage for everyone who needs it.

Now more than ever, individuals need to be proactive about protecting their homes and property from wildfire risks. As insurance agents, this is perhaps the best advice we can give to our clients as we continue to adapt to changes ourselves.

Ben Jones is marketing manager at Dryad. Dryad provides ultra-early detection of wildfires as well as health & growth-monitoring of forests using solar-powered gas sensors in a large-scale internet of things (IoT) sensor network.

This month’s issue

The August issue is out now!