4 Myths and Realities About the 2023 M&A Environment

By: Brian McNeely

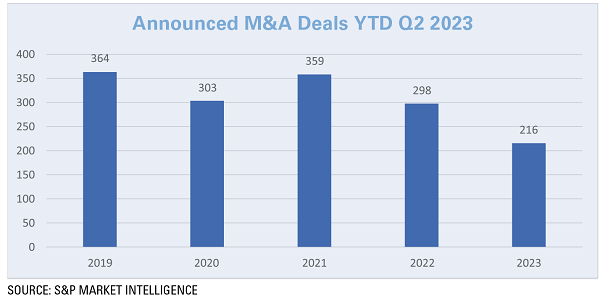

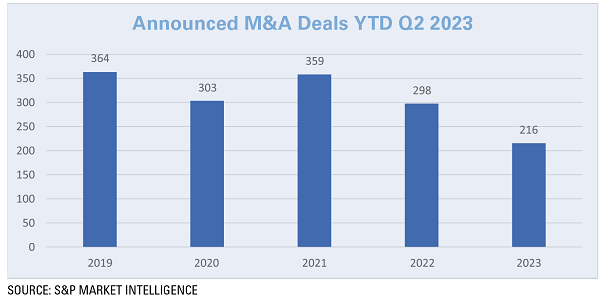

Over the past 12 months, any mention or discussion of agent and broker mergers & acquisitions has been accompanied by data showing a material decline in the number of transactions. In 2022, the number of transactions was the lowest since 2016, a trend that has continued in 2023.

Over the past 12 months, any mention or discussion of agent and broker mergers & acquisitions has been accompanied by data showing a material decline in the number of transactions. In 2022, the number of transactions was the lowest since 2016, a trend that has continued in 2023.

While it is true that the number of transactions has declined, it’s easy to draw some incorrect conclusions about the current state of the M&A market. Here are four common myths and the realities:

Myth 1: Interest rate increases are impacting everyone equally. Nobody needs to be reminded that interest rates have increased materially. While this can have broad implications for agents and brokers, from an M&A perspective, it impacts the cost to finance acquisitions and the purchase prices that can be paid.

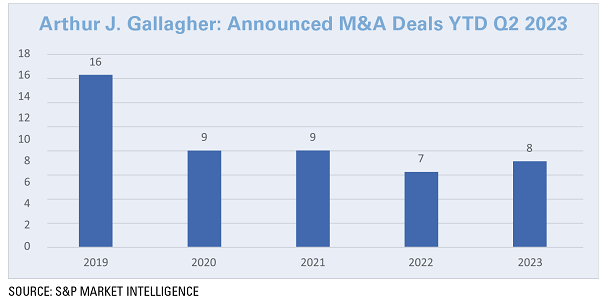

All the active buyers in the market have different capital structures, such as some with more debt than others and debt terms that vary widely. As a result, there are several buyers that have little debt or at least favorable terms associated with their debt. For those buyers, their already strong appetite for acquisitions has not changed. One example is Arthur J. Gallagher, a public broker and one of the more active buyers, which is maintaining the same pace of acquisitions in 2023 that it did in 2020.

Myth 2: Valuations have decreased. “If activity is down, valuations must be down.” Not true. In fact, it can be argued that valuations have increased slightly for the largest, best assets.

Why is that the case? It is basic supply and demand—there are still a large number of active acquirers and a limited number of available sellers.

Myth 3: Market enthusiasm is waning. The industry’s financial performance is perhaps the best it has ever been. Largely driven by the hard market, organic growth is at an all-time high for the industry and this organic growth is contributing to record profitability levels.

The capital markets continue to take note, with new players determining how they can enter the market and some existing players evaluating how they can expand their presence.

Myth 4: Fundamental issues for some sellers have changed. There are a multitude of reasons why an independent agent or broker decides to partner with someone. However, one of the most frequently cited reasons is the need for tools and resources to remain competitive in the market. This still holds true, but there is a larger issue. Many firms continue to struggle to recruit, train and retain the best talent. Talent is critical to the success of a firm, and many firms are struggling to resolve this issue.

Is deal volume down? Absolutely. However, many of the acquirers that have issues and have materially reduced their activity were the ones that did the largest volume of transactions. There are still many acquirers active in the market who are as hungry as ever, and the competition among that group continues to drive high valuations.

Brian McNeely is a partner at Reagan Consulting.

This month’s issue

The May issue is out now!