Independent Agency Valuations: Why Revenue Multiples Are Misleading

By Craig Niess

In insurance industry circles, there is a certain industry parlance tied to an independent agency valuation. Agency owners have historically thrown out numbers such as “I am worth X times revenue.”

Many buy-sell agreements will incorporate language that stipulates that the value of the agency will be determined in such a manner at the time of a sale or when settling an estate. Historically, the benchmark that was bantered about was 1.5 times revenue, but over time, the discussions evolved to where 2 times revenue became the standard multiple.

This evolution was mainly due to the feeding frenzy in the merger & acquisition space over the past 10 years. A large influx of private equity (PE) money drove up agency values. A large influx of cash, coupled with a stagnant number of independent agencies, triggered the law of supply and demand. High demand plus low supply has led to all-time high pricing.

More From the July Issue

By using industry lore to establish the value of your agency, you may be inflating the value of your agency or, worse, shortchanging yourself on what is likely your greatest financial asset. An independent agency valuation is the key to determining your agency value, and can also help you understand what levers you can pull to increase value over time.

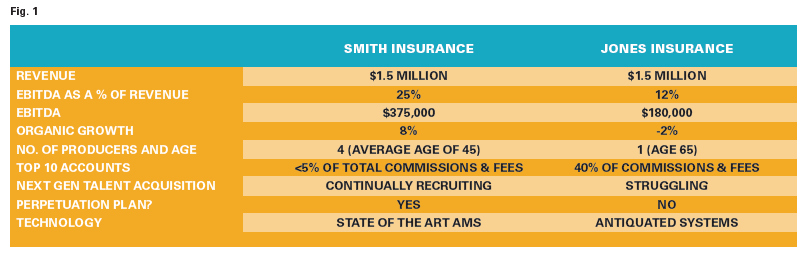

To illustrate how an agency’s value is more complex than an “X times revenue” calculation, consider two agencies in Figure 1: Smith Insurance and Jones Insurance. The agencies seem similar, but, upon closer examination, turn out to be wildly different.

Each agency earns $1.5 million in revenue and each agency believes that they are worth $3 million, which is 2 times revenue. But, as we look more closely, we see that the agencies are vastly different in how they manage their operations, how they compensate their employees, and how they drive growth and efficiencies. These differences create a wide disparity in value.

The salient components of agency operations indicate that these agencies are vastly different and would command a very different price.

Using the 2 times value rule of thumb, Smith Insurance would be greatly undervalued, while Jones Insurance would be greatly overvalued.

Smith Insurance is running its agency like a business. An EBITDA (earnings before interest, taxes, depreciation and amortization) margin of 25% suggests it is exercising expense controls. The 12% margin for Jones Insurance suggests its expense loads are out of control—or, perhaps, that the owner is running the agency as a lifestyle. While there is nothing inherently wrong with a lifestyle business, these low margins will give some buyers pause.

Furthermore, Smith Insurance is outperforming Jones Insurance in a number of key metrics: organic growth, key accounts, perpetuation planning and investment in next-generation talent. Any buyer comparing these two agencies would value Smith Insurance more highly than Jones Insurance.

This is why the one-size-fits-all technique for valuing agencies is highly inaccurate. The multiple of revenue technique is an expression of value, while an agency valuation is a calculation of value. When you are ready to realize the value of your agency and your life’s work, do you want to value it on the back of a napkin, or take a deeper dive with a proper agency valuation?

An agency valuation will determine your value, which will form a good baseline for you to consider as you move forward. However, it’s important to keep in mind that value is different than pricing. Given the current M&A climate, an agency could sell to an external buyer at a price much higher than the valuation. This can be influenced by a buyer’s appetite for a certain geography, niche or access to certain carriers. Additionally, an agency owner might sell at a discounted price to family or key employees to help facilitate the deal.

Examining agency financials discovers things such as growth rates, non-recurring revenues or expenses, and any expenses that are not essential to running the day-to-day operation, such as a spouse’s car, family cellphone plan or country club memberships.

After examining these financials and making adjustments, we arrive at a pro forma EBITDA number. This number is indicative of the profit a third-party buyer could expect to pull out of the agency after adjusting and right-sizing expense loads. Then, a risk assessment of the agency informs the valuation multiple. By examining the risk of the agency, we get a true picture of the risk of the agency.

Items considered include:

- Owner age and perpetuation plan

- Growth

- Payroll and staffing

- Carrier mix

- Key accounts

- Producer and employee contracts

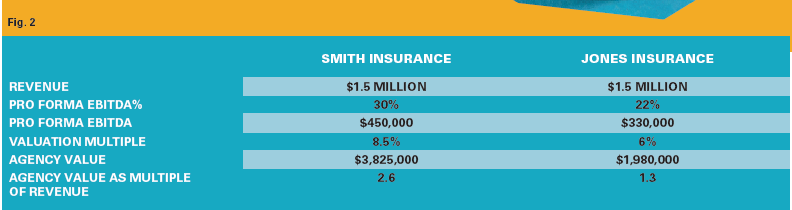

The independent agency valuation multiple is ratcheted up or down based on the strengths and weaknesses of each of the risk factors. As you can see in Fig. 2, this has a large impact on the value of an agency.

The calculation of the value of each of these agencies shows the wide discrepancy between agencies that are the same size but have vastly different characteristics. Smith Insurance performs at a high level and has much lower risk than Jones Insurance. By investing in growth and operating as a business versus a lifestyle, it is positioned to maximize its value.

Timing is key. We encourage agencies to not only get a valuation, but to do it sooner rather than later. An agency owner who has one foot out the door and then decides to get a valuation will not be in a position to maximize their value. An owner who gets a valuation well before exiting the business will not only understand their value, but they will have enough runway to institute changes to increase the value prior to their exit.

Craig Niess is director of business planning and valuations at IA Valuations.

If you see similarities between your agency and either the Smith or Jones agencies in these examples, now is the time to act. Please reach out to contact@iavaluations.com to help your agency reach its fullest potential.

Founded in 2017, the IA Valuations team has performed over 270 valuations to independent insurance agencies across the U.S. Our advisers have 25+ years of experience guiding agency owners on maximizing their agency value, planning and legal needs for ownership transition.

The information provided is general in nature and shall not be construed as personal legal, tax or financial advice for your situation. Email contact@iavaluations.com to discuss your personal situation.

Copyright ©2025 by IA Valuations and Ohio Insurance Agents Association (OIA). All rights reserved. No portion of this document may be reproduced in any manner without the prior written consent of IA Valuations or OIA. In addition, this document may not be posted as a link on any public or private website without the prior written consent of IA Valuations or OIA.

Categories

Agency Management Solutions

This month’s issue

The July issue is out now!