How Industry Changes Are Influencing, But Not Deterring, M&A Activity

By Brian Deitz

Organic growth in the industry is declining, following changes in property & casualty insurance pricing. Artificial intelligence (AI)-based distribution of personal lines has arrived, with Insurify and Tuio launching the first ChatGPT-powered insurance comparison apps. Public broker stock prices are struggling mightily, hit hard by both lower organic growth and a rash market reaction to the Insurify and Tuio announcements. And there has been talent poaching at an unprecedented scale, with large teams of brokers and insurance professionals switching firms.

And yet, despite all the noise, the mergers & acquisitions market remains active. As we move into the middle of 2026, the demand for broker acquisitions remains strong. While some of these recent trends have influenced the deal marketplace, it certainly hasn’t been interrupted.

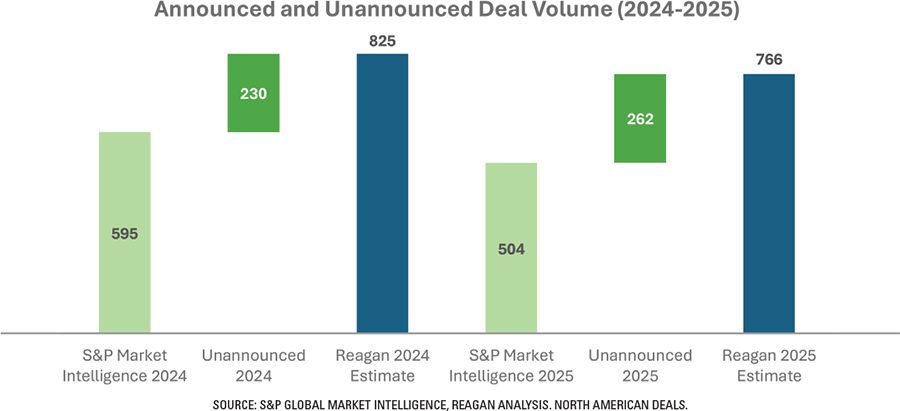

Deal activity in 2024 and 2025 did not surpass the high-water mark for the insurance distribution industry, but it wasn’t terribly far off. Based on Reagan’s analysis, there were 825 deals done in 2024 and 766 in 2025, down from the industry’s all-time high of 983 deals in 2021 but still a healthy level of activity.

However, an increasingly large number of these transactions were not announced publicly. S&P Global Market Intelligence, the long-standing tracker of insurance distribution deals, reported only 595 deals in 2024 and 504 in 2025.

Why the discrepancy? Some deals just don’t get reported due to the buyer’s size or materiality. However, many established acquirers are not publicizing transactions to reduce the risk of talent poaching from other industry players.

This trend started a few years ago and has accelerated recently. Because a change of control can be destabilizing to employees, several experienced purchasers of agencies are choosing not to advertise to their competitors that there is talent that is potentially up for grabs. With several of the industry’s largest players no longer announcing their transactions, deal totals are significantly understated versus reality.

Announced or unannounced, large brokers are still buying, and despite public broker trading multiples, they are still paying historically high prices for their M&A targets, though not quite as frequently as in the past couple of years.

We have seen buyers exercise more pricing discipline this year than in past years, reserving the highest valuations for sellers that outperform the industry with actionable scale, specialty capabilities and demonstrated organic growth.

More on M&A

For firms with these qualities, valuations are staying strong. For targets with more average performance characteristics, reaching top-tier valuations depends on finding a partner with meaningful synergies, such as product capabilities, leadership teams in key geographies or revenue and cost savings. Higher valuations are still available but are likely to attract a smaller number of buyers and are more situation-dependent.

M&A volume in 2026 will remain strong. Most important in understanding these trends is appreciating that the fundamentals of consolidation are unchanged. We are operating in a fragmented industry where there are significant benefits to scale. There are still over 35,000 independent agents and brokers in the U.S.—even after a decade of 500 or more acquisitions per year. And the advent of AI and its applications on integrating businesses may make the advantages of scale even easier to achieve. Temporary fluctuations in organic growth and public market valuations won’t halt those dynamics.

Brian Deitz is a partner at Reagan Consulting.

Agency Management Solutions

Insurance Markets

This month’s issue

The June issue is out now!