Why the E&S Market Continues to Grow

The hard market is among the causes of the growth of the excess & surplus market, which had previously been considered a safety valve.

The hard market is among the causes of the growth of the excess & surplus market, which had previously been considered a safety valve.

The coverage allows small business owners with multiple locations to easily secure coverage through a single policy.

Despite the softer market conditions, the marine insurance industry—marine cargo, inland marine, and marine hull and liability—continues to be impacted by evolving trends.

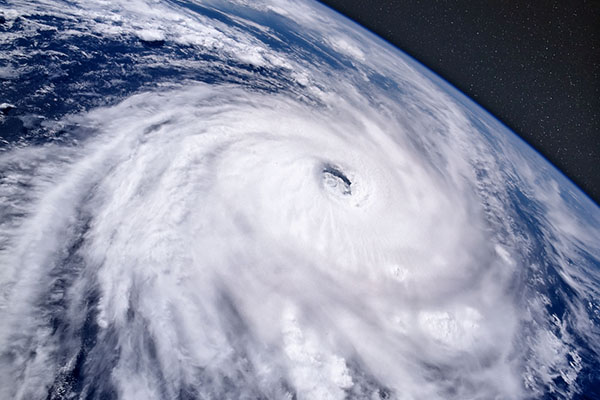

Coral reefs, mangroves, salt marshes and seagrass meadows can significantly reduce flood losses in coastal areas, according to a Swiss Re Institute analysis of data.

Key highlights include flexible policy options and a multitude of deductible and coverage options, many of which are unique to boaters.

As insurers increase their underwriting restrictions to limit storm exposures, risk mitigation is becoming more important than ever for commercial insureds.

Cannabis operators are facing increasing operational costs and liability risks and are looking to cut costs wherever they can.

The guidelines for the federally funded program include maintaining properties in compliance with local housing codes, passing periodic inspections by housing authorities and following strict eviction and lease termination procedures.

Challenges persist for the cannabis industry due to changes in the regulatory landscape, an increase in product recalls, increasing premiums and industry consolidation.

The coverage features a data-driven trigger, which removes the need to prove a covered loss or damage.