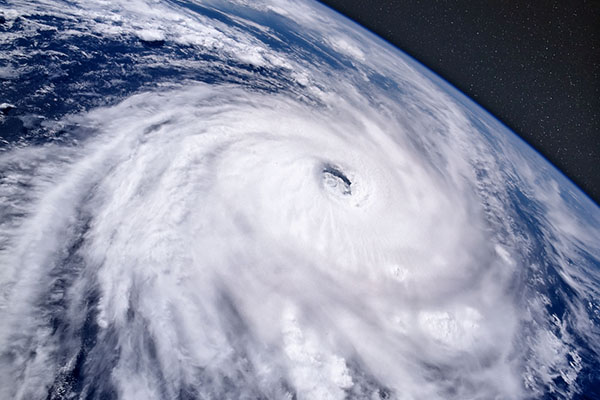

How Agents Can Help Clients Navigate Growing Flood Risks

As flood risk becomes more complex and less tied to traditional flood maps, agents play a key role in helping customers understand their real exposure.

As flood risk becomes more complex and less tied to traditional flood maps, agents play a key role in helping customers understand their real exposure.

The product covers any economic losses resulting from fluvial, pluvial and coastal flooding, and offers rapid payouts triggered by pre‑set conditions.

From hurricanes in the Southeast, wildfires in the West and severe convective storms in between, catastrophes are a defining feature of the current insurance landscape and are changing property insurance.

Nearly 85% of single-family homes at risk of flooding in the U.S. carry insufficient coverage, leaving households vulnerable to thousands of dollars in out-of-pocket costs, according to Neptune Flood.

The endorsement is designed for homes outside historical high-risk flood zones and provides coverage for damage from flood waters or surface waters.

Proactive conversations with clients about catastrophe risks can surface potential coverage gaps and open the door to more forward-looking planning.

This year’s hurricane season, which started on June 1, has a 60% chance of above-normal activity, with 13 to 19 named storms expected.

Coral reefs, mangroves, salt marshes and seagrass meadows can significantly reduce flood losses in coastal areas, according to a Swiss Re Institute analysis of data.

As insurers increase their underwriting restrictions to limit storm exposures, risk mitigation is becoming more important than ever for commercial insureds.

Colorado State University (CSU) hurricane researchers are predicting 17 named storms during the Atlantic hurricane season.