What Consolidation Means for the Independent Insurance Agency System

By: Jeff Smith

It is undeniable that the independent agency system is undergoing massive consolidation. In what many have dubbed “the greatest wealth transfer in the history of the independent agency system,” we are witnessing a realignment of the independent insurance agency business model.

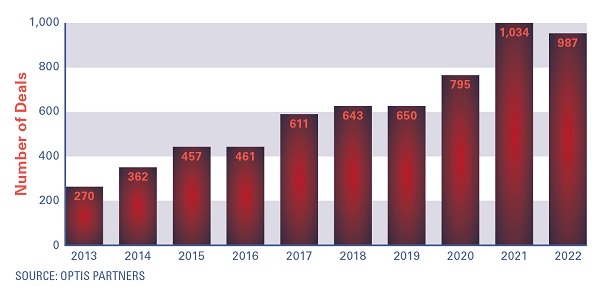

Over the past 10 years, the independent agency system has experienced a 250% increase in the number of reported merger & acquisition transactions, according to Optis Partners. In that period, 6,270 M&A deals have been announced, which is likely only one-third of the actual ownership transactions taking place in the independent agency system.

Between unannounced external sales, internal sales and perpetuations, there were tens of thousands of additional ownership transitions in the marketplace over the past decade—with many more forecasted over the next 10 years.

While we do not anticipate M&A to ratchet up, we do expect the level of transactions to remain at 2017 levels and above. This is being fueled by unprecedented investment of private equity (PE) dollars in the independent agency system, an increasing number of PE buyers, an aging ownership population and a healthy number of agencies in the system. This means the independent agency channel will experience an even greater consolidation in the coming years as the big PE buyers continue to get bigger.

As an independent agency owner, you are likely wondering what this means to you, your long-term financial well-being and the value of your agency.

Independent agencies are not the first profession to experience industry consolidation driven largely by PE and the evolution of the business model. Many other mature industries have experienced the same fate, including medical, dental, pharmacists, nursing homes, law, accounting, financial advisers and auto dealers.

To understand what independent agencies are experiencing, look no further than your book of business and the accounts you have lost to M&A over the past decade. You will likely identify clients that were in mature businesses in traditionally stable industries that produced consistent profit margins and underwent some degree of change due to technology and economic evolution. Those lost accounts are likely going through similar consolidation experiences in their industry.

Commonality with Health Care Consolidation

In my professional experience and area of expertise, the consolidation of independently owned medical practices and hospitals has been noticeable. I worked in the health care industry 20 years ago and witnessed the medical profession as predominantly independently owned medical practices and hospitals. In the early 2000s, we started to see some consolidation. Little did we know it was just the tip of the iceberg.

Fast forward to 2023 and the majority of medical practices are now owned by health systems, physicians are employees of those health systems, and local hospitals are almost extinct because most have been consolidated under several multibillion-dollar health system brands.

For those of you who have experience insuring local medical practices and hospitals, you have likely experienced this consolidation firsthand or are anticipating that it could happen to you at any moment. Understanding what drove this consolidation will help us further understand what it means to the independent agent system.

For starters, health care is a $4.3 trillion industry and is continuing to grow. PE investors take notice of this and invest their resources in growing parts of the economy.

There were many inefficiencies in how independent medical practice and hospitals were developed and most needed modernization to meet the demands of an increasingly complex health care system. The industry was largely paper based, disconnected and incredibly complex for patients to navigate. Technology is rapidly changing this with electronic medical records, customer portals and other tools to empower patients.

Physicians are medical practitioners first and foremost. Their focus is on patient care, not the business of running a medical practice. Any entity that can eliminate the challenges and pressures of running a medical practice were met with enthusiasm. And while health care is a growing industry, it is under constant cost-cutting pressures. Patients, politicians, employers and health insurers are all constantly advocating for relief from ever-increasing health care costs.

PE, health systems and other consolidators stepped in to take advantage and solve many of these challenges. In the process, the entire health care system has undergone a fundamental realignment of its business model.

Consolidation in the System

While the independent agency system is different from health care in many ways, the consolidation parallels we are experiencing are similar. Consolidation is upon us, and it is fast and big, complex and sophisticated, and disruptive and efficient. There may be moments where it feels like things are quiet and calm, but make no mistake—we are under a massive consolidation effort that is fundamentally altering the independent agency business model.

The independent agency system is massive. The U.S. property & casualty market alone is comprised of an estimated $890 billion in premium and growing by 8% per year. Simultaneously, the independent agency system has traditionally been highly inefficient, segregated by proprietary systems and largely paper based.

Insurance agents, while entrepreneurial, tend to be risk advisers first. Many agents enjoy assessing risks, selling the insurance product needed for their clients and then moving onto the next opportunity. Many agents do not like the responsibility of managing employees, financials, marketing, technology systems and the other duties of running a business.

Further, while the independent agency system continues to grow, there are increasing pressures on agent commissions and profit-sharing agreements with carriers. With carriers experiencing mounting profitability challenges, it is trickling down to agents to figure out greater efficiencies to remain profitable.

All this leads to the perfect environment for industry consolidation. Insert PE investments, and now you have all the resources to consolidate an entire industry in a few short decades.

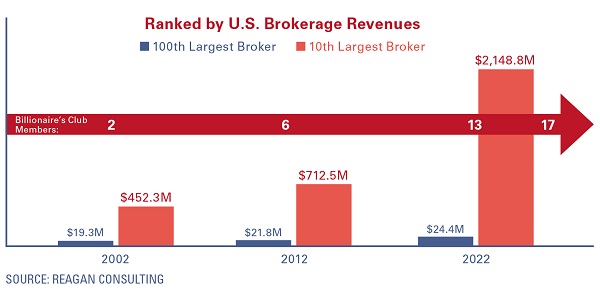

This is unquestionably happening as we watch the big get demonstratively bigger. As evidenced by the graph compiled by Reagan Consulting, there are now 17 $1 billion brokers, whereas 10 years ago there were six. It is no longer like flipping homes for short-term gain. Many of the PE buyers are now advancing with both an acquisition and organic growth-oriented mindset.

While we are not yet in the midst of the “why buy your business when I can take your business” phase, as the PE buyers scale, they represent a new competitive threat that retail agencies have not experienced thus far.

What Does This Mean to Independent Agency Owners?

What Does This Mean to Independent Agency Owners?

Your agency has great value, and that is unlikely to change anytime soon. The infusion of PE money and massive consolidation has resulted in record agency valuations. Your agency is likely worth double what it was 10 years ago just due to the market factors and conditions we have experienced. As long as your agency is growing profitably, you will continue to see your value increase in the coming years. The type of business you write will likely become a greater factor but, as of now, profitable growth is paramount to agency value.

In this era of consolidation, it is very important to know your strategy for growth and long-term viability if you choose to remain an independent insurance agency owner. The pressures to manage and lead your business effectively will become more important as competitors take different shapes and sizes. That means you must continue to grow organically, achieve consistent profitability margins and have an active relationship with technology.

In this endeavor, you need a documented transition plan that you revisit annually. Whether you are an agency owner in your 30s or 70s—or anywhere in between—it is important to have a written transition plan that spells out your plans from year to year. The market is changing quickly, and agents are changing their minds quickly. A plan that is your true north will help you stay focused on playing the long game.

It is also important to uderstand the current fair market value of your agency, future projected earnings and risk factors in your agency. It is likely you are already fielding calls about selling your agency. If not, they are coming. Every PE buyer in the marketplace has field staff, such as recruiters and headhunters, whose sole responsibility is to identify good acquisition targets, develop relationships and pursue opportunities. Take the opportunity to listen to the pitch and learn about the market, but remember to circle back to your documented plan and evaluate whether it connects with where you are headed.

Consolidation in our industry is real. Every part of the insurance industry and independent agency system is being affected. It is outside of our control and the scope of most retail agency owners. The independent agency system will look significantly different in 5-10 years as consolidation continues to play out.

Despite the consolidation, it is a great time to be an independent agency owner. The independent agency market continues to increase year over year, billions of dollars are being invested annually to grow the system, your asset has doubled in value, and there are now more options than ever before to transition your agency.

Jeff Smith is CEO of the Ohio Insurance Agents Association.

This month’s issue

The June issue is out now!