Strategies for Going Beyond P&C and Into Employee Benefits

By: Will Jones

Less than 15% of independent insurance agencies planned to start selling individual life, annuities, mutual funds and other investment products in 2022, according to the 2022 Agency Universe Study. Even fewer—10% or less—planned to start selling group or medical insurance, group life and other employee benefits, such as dental, vision and disability.

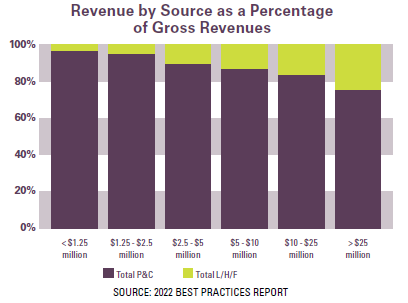

However, growing agencies are increasing revenue through these lines of insurance. As outlined in the “Revenues by Source as a Percentage of Gross Revenue” chart, the 2022 Best Practices Report shows that as agency revenue increases, the percentage of gross revenue from life, health and financial products increases.

Independent insurance agents and brokers dominate the commercial property & casualty market—an 88% market share, according to the 2022 Big “I” Market Share Report—which makes the employee benefits space a new frontier for many agencies.

In 2011, Quincy Branch (pictured) started to lay the foundations for Branch Benefits Consultants. Originally, the company was a wing of the agency his father co-owned, but Branch eventually purchased what he’d built before later buying the commercial and personal lines business, as well.

How did he do it? “It starts with infrastructure first and foremost,” says Branch, CEO of Branch Benefits Consultants in Las Vegas, who notes that carrier appointments are “not as difficult to get as they are in commercial insurance.”

Still, human capital and expertise are essential to success in this area. Branch acquired the Registered Health Underwriter (RHU) and Employee Healthcare Benefits Associate (EHBA) designation “because I wanted to make sure that I was as educated as possible,” he says. Further, as a young leader of a brand-new benefits division, “I wanted people, especially the people that worked for me, to know that I knew what I was talking about.”

When it came to hiring a team, Branch attracted insurance professionals who faced barriers to career growth with their existing employers. “We were able to find talent that wasn’t being utilized the way they wanted to be utilized,” he says. “We gave them an opportunity to showcase their talent.”

Serendipitously, a year before Branch Benefits Consultants was founded, Congress passed the Affordable Care Act (ACA). To meet the demand for individual policies, Branch built a department dedicated to the niche. “We had a compliance division and a whole wing of three or four people where that’s all they did,” he says. “We became a local expert.”

Changing Perspective

At first, Branch grew the commercial benefits book through referral partnerships. “It was a market that not a lot of my other colleagues in our local area were in,” Branch says. “They knew I wasn’t going after their commercial business, so didn’t mind if I talked to their clients about benefits.”

After using benefits to grow their reputation, Branch Benefits Consultants became a full-service agency when they acquired Branch, Hernandez and Associates, which was co-owned by his father, Aubery Branch, and Joe Hernandez. At that point, Branch was faced with a mountain of opportunities to cross-sell benefits to the existing commercial lines book. However, he first needed to determine a strategy.

“It wasn’t about identifying what markets we wanted to go after,” he says. “It was about looking at the internal markets to develop a strategy on how we were going to market and advertise to those businesses that we’ve already built trust with. It’s like, why go out and recreate the wheel when you’re already sitting on a gold mine?”

While sitting on a gold mine may sound enticing, investing resources to turn that gold into revenue takes commitment. If your agency is trying to figure out if it’s a financially viable strategy, there’s good news: “You don’t have to jump in with both feet,” says Todd Villeneuve, managing partner, IFC National Marketing.

“Start with an informal survey of your clients to find out if they are looking for a better or more cost-effective solution,” Villeneuve explains. “Some might say they’re already working with someone, in which case you should consider building a partnership with them, especially if they’re recognized in your area.”

For insurance salespeople, generating interest and demand from clients is the easy part. It’s the expertise that is more difficult to find. But rather than attempting to be a jack of all trades, “you can borrow expertise,” Villeneuve says, noting that IFC Marketing provides independent insurance agencies with expertise on a temporary, full-time basis to help p&c agencies expand.

“Once you have a tactical referral relationship and you start splitting commissions, you start to see what that revenue stream creates and justify hiring people,” he adds.

Agencies can also look to new carrier partnerships as they expand beyond p&c insurance for guidance and resources. Before building a partnership, agencies “should consider the carrier’s product offerings, as well as the solutions they can provide to help implement and retain enrollments,” says Andrew Story, senior broker development consultant at Aflac.

“A good place to start is with questions such as: How will our client be educated on the new products? How will employees sign up? What does the client need and expect, including reporting, post-enrollment communication and claims?” Story says.

Branch Benefits Consultants started writing benefits for small and medium-sized businesses but now mostly writes mid- to large-sized groups. While Branch did not need to recreate the wheel, he still needed to build the mechanics around the p-c and benefits offerings to ensure any attempted cross-sell didn’t upset the client relationship.

“While the idea around the cross-sell sounds amazing and makes sense, it’s not as easy as it sounds,” Branch says. “As an agency, we have had to build trust and buy-in between departments to make sure that, at the end of the day, our goal is to wrap ourselves around a client.”

“Some things go hand in hand, like workers compensation and health care. But how do you make sure both accounts are collaborating? It’s not as easy as throwing the ball out to go play,” Branch continues. “It’s a dance. You have to be intentional about how you put that structure in place.”

Healthy Discussion

For businesses and employees, medical insurance is the foundation of their benefits package. Outside of leave policies, such as maternal, paternal, sick and vacation, and the opportunity for a flexible workday, offering robust health insurance is an important recruitment and retention tool for employers, especially considering the high level of employee attrition in 2021 and 2022, according to McKinsey.

Will “Bull” Belletto, employee benefits agent at WAFD Insurance Group in Albuquerque, New Mexico, built his reputation in his community by joining nonprofits and charity organizations and networking. “Those are leads you can never get by smiling and dialing,” he says. “If you are there for the greater good of your community, people will listen to what you have to say.”

Belletto sells health insurance, dental, vision, worksite benefits, group disability and group life. “My aim is to provide value to these people by helping them solve their business problems,” he says, and one of the biggest problems Americans and employers face is health care.

Employer-sponsored health insurance covers nearly half of Americans, according to the Kaiser Family Foundation (KFF). But over the past decade, employer-sponsored insurance health care premiums have risen above the rate of inflation and have outpaced wage growth, according to Mercer.

In 2021, the average cost of employee health insurance premiums for family coverage increased by 4% from the previous year to $22,221, according to KFF. These premiums for families and individuals have increased 22% over the last five years and 47% during the previous 10 years. The rising cost of health care, rather than utilization, has led to the increases. The health insurance market has responded with high-deductible plans and rising copays, which pass a portion of the increases onto the insured.

Meanwhile, it isn’t only employees who are being squeezed by rising premiums. In 2021, KFF found that the average health insurance cost for employers was $16,253 annually, or 73% of the premium, to cover a family and $6,440, or 83% of the premium, for an individual.

When Belletto works with employers, he learns how the company operates and accesses health care, and can then “start making recommendations on self-funding and pulling different levers to get these costs under control,” he says.

A self-funded plan involves an employer assuming all the costs for their employees’ health care expenses. An insurance company manages the payments, but the employer pays the claims. In some cases, it is a cheaper option than traditional group plans. Employers pay a monthly amount and, if any funds are not spent at the end of the year, they are returned to the employer.

A self-funded plan also gives employers a choice of network provider, which often means that “the first change always comes with bringing in a direct primary care company that gives people unlimited access,” Belletto says.

Providing “access” involves two solutions to overcome obstacles. First, telemedicine, which increased in use 15x from March 2020 to February 2021, according to the Government Accountability Office, can give insured a phone or video consultation within 20 minutes, depending on the provider. Second, with high levels of burnout in the medical profession affecting wait times, electing a provider with a higher number of available physicians speeds up the time it takes for an ailment to be addressed and ensures an employee’s speedy return to work.

“There are many different alternative funding programs that are available, and all should be evaluated,” agrees Chris Fiorello, employee benefits practice leader—Upstate New York at USI Insurance Services. “Changing the funding of the plan is an important step that has many advantages, but it can have disadvantages and financial pitfalls. A full analysis should be done to determine what funding source is right for the client and ensure they’re not taking on too much financial risk.”

“We have an analysis that goes back five years to determine whether self-funding would’ve worked against their current funding and then use predictive modeling to go forward five years,” he says. “It’s a great way to determine over a period of time, not in a single year renewal, if self-funding makes financial sense against a more traditional insured model.”

One of the biggest medical expenses for insureds is pharmacy costs. The cost of specialty drugs totaled $301 billion in 2021, an increase of 43% since 2016, according to the U.S. Department of Health & Human Services. Meanwhile, specialty drugs—used to treat complex chronic conditions, such as cancer, rheumatoid arthritis and multiple sclerosis—represented 50% of total drug spending in 2021.

Specialty drugs often cost $1,000 or more per month—and spending on them is growing 15%-20% per year, according to healthinsurance.org. Traditionally, Fiorello’s division focused on high-cost inpatient types of expenses. However, over the last several years, they have focused more heavily on pharmacy spending. The niche is currently so important that USI has pharmacy consultants on staff to “effectively and sustainably manage their clients’ pharmacy contracts to ensure the client is properly protected and has the best financial outcomes,” he explains. “It’s now 25%-35% of the total expense of an employer’s health plan. It must be properly managed.”

“We understand the importance of this and have developed our own internal Pharmacy Consulting Practice, but smaller agencies could use outside pharmacy consultants as well,” Fiorello says. “However, agents need to be cognizant of where they’re getting their advice. There are competing interests out there and you need to be sure that you are getting unbiased support or advice—that’s why we developed our own team.”

Another costly but emerging trend in the medical insurance space is gene therapy, which replaces a faulty gene or adds a new gene in an attempt to cure disease or improve the body’s ability to fight disease. In doing so, new technology is changing the way medical professionals treat cystic fibrosis, Tay-Sachs disease, sickle cell anemia and cancer, among other diseases.

“There continues to be incredible breakthroughs in gene therapies,” Fiorello adds. “That said, it feels like we may be going too fast and don’t know the efficacy and long-term effects of these therapies. What we do know is that they carry a very big price tag. Understanding this emerging care, the expense and liability of the plan and how to control it is a very important process that consultants and ultimately employers should focus on.”

Frame of Reference

While the medical benefits represent the largest amount of commission payable to the agent, some accounts require patience. And whether you are going after their medical, p&c, voluntary benefits or the whole lot, a tailored approach is always the best way to go.

“If I’ve been referred to a company and they have everything, I’m going to try to take everything because they might as well make me their single point of contact,” Belletto says. “But a new company with around 15 employees, for example, may not know if they can afford certain benefits but understand they need to offer their employees something, and that’s a different prospect.”

“In those cases, we’ll start with dental and vision, which is around $50 for both, and then a group life insurance policy, which is so cheap: For $60 per employee per month, they can have a benefits package,” Belletto explains. “Once they learn how to manage that and get used to it—because there’s a lot that goes on the employer and employee with managing it—you can start to introduce more complex solutions.”

However, “if an employer wants to show that they care, putting in an employee assistance program (EAP) program—and making sure that they advertise it—is key,” Branch says. “There’s not a person on this planet that’s not stressed out, overworked or dealing with multiple things, both personally and professionally. A solid EAP program gives employees a resource.”

Distractions, such as marital, family, financial or emotional problems, may hurt productivity and drive up costs for businesses, according to the Society for Human Resources Management (SHRM). “EAPs can help employers reduce absenteeism, workers’ compensation claims, health care costs, accidents and grievances. In addition, they can address safety and security issues, improve employee productivity and engagement, and reduce costs related to employee turnover,” SHRM guidance says.

“Whether it’s counseling, concierge services, looking for an attorney or whatever the case may be, there are so many different things that people need,” Branch says. “An employer can’t be everything to everybody, but they can at least give them access to something that they wouldn’t have otherwise.”

One of the most “distracted” cohorts in the workplace is the “sandwich generation,” which is defined as people, typically in their 30s or 40s, responsible for bringing up their children and for the care of their aging parents.

Every day until 2030, 10,000 baby boomers will turn 65, and 7 out of 10 people will require long-term care in their lifetime, according to the U.S. Department of Health and Human Services. Meanwhile, a national problem—the affordability, accessibility and quality of child care—costs the U.S. economy $122 billion in lost earnings, productivity and revenue every year, according to a report from the bipartisan Council for a Strong America. Employers whose benefits meet these needs of the sandwich generation are well-positioned to retain productive employees.

“We’re starting to see more interest in finding help for elderly care. More employees are reaching out for additional support for their loved ones,” says Ashley Engl, employee benefits client success account executive at Lawley in Buffalo, New York. “For childcare needs, there are providers that can connect employees to a network of specialists that will give them access to services to help them manage their situation.”

Also, as more baby boomers retire, employers should review their benefits package so it appeals to the under-40 population. After living through the second of two major economic crises during the pandemic, older millennials delayed having children, according to a Harris Poll. “So, in the 30-40-year-old population, there has been more interest in fertility services and other related services that health insurance may not cover,” Engl says. “The best benefits package should be centered on what the employees are looking for and that can change based on the demographics.”

And with 27% of the workforce expected to be from Generation Z—born between 1997 and 2012—according to the World Economic Forum, and the average loan debt for a bachelor’s degree among the class of 2020 sitting at $28,400, according to the most recent data available from College Board, student loan repayment programs are another benefit that employers may be interested in offering.

“If there’s one thing that the pandemic has taught us, it’s that life happens,” Branch says. “The voluntary space is ripe because you can give employers the chance to offer their employees life or disability insurance for themselves or a family member.”

“With multiple generations in households, you can have those long-term conversations,” he says. “There are other opportunities to put other voluntary opportunities in place, but dental is a great door-opener because they’re not big disruptors.”

Field of Vision

With the threat of a global recession in 2023, employees are understandably concerned about their financial futures. However, employers can provide employees with tax sheltered accounts that will help employees stretch their salary.

Tax sheltered accounts include health savings accounts (HSA) for medical expenses; flexible savings accounts (FSA) for certain medical costs, child care and other health services; and lifestyle savings accounts (LSA), a newer employee benefit, which can cover things defined by an employer but which includes costs related to physical, financial and emotional wellness. All of these can stretch employee pay and support staff.

“There are many different spending accounts that are available to the employees, but the biggest thing is to not just consult with the employer, but to truly connect with and educate the employee,” Fiorello says. “Employees typically don’t have a good understanding of the taxes they pay. Their income taxes just come out of their paycheck, and they file their tax returns once a year. Because of this, the understanding of the tax advantages of these types of accounts is often missed. Our team spends a significant amount of time with employees educating them on the financial benefit of these accounts.”

Education relies on helping employees understand different restrictions, such as what you can use the account for, if a balance will rollover into a new calendar year or whether they have to “use-it-or-lose-it.” Crucially, “the employee has to be engaged and understand it for it to work,” Fiorello says. “Where it really starts to work is when one or a few employees take advantage of it. Then they start talking about it with their colleagues and soon you have a domino effect—slowly but surely there’s more and more participation.”

But increased employee engagement with their benefits isn’t the only positive. “There’s also a benefit to the employer, because the majority of these accounts means the employer doesn’t have to pay the FICA match,” Fiorello points out, which is 6.2% of the employee’s first $160,200 of income in 2023.

But of all the financial savings vehicles offered by employers, a traditional 401(k) is by far the most popular, offered by 95% of employers, according to the SHRM “Employee Benefits Survey.” Meanwhile, 68% offer a Roth 401(k). Many employers also provided some type of employer match to those retirement plans, with employers providing an average maximum percentage salary match of 6.8% for traditional 401(k) plans and 6.7% for Roth 401(k) plans, the study found.

Before Fiorello sold his firm—which had 15-20 employees and mainly dealt with small to midsize employers—to USI, he had relationships with financial advisers. “It worked well because we were rounding out our clients together and providing synergistic consulting that was much needed,” he says. With USI, which is among the 20 largest brokerages in America, the company has its own division dedicated to financial services.

However, doing pensions and other financial investments in-house comes with a warning due to compliance and regulation. “There’s more compliance in that arena than there is with p&c or employee benefits. It’s an understandably very regulated portion of the industry,” Fiorello adds. “There’s a fiduciary responsibility for employers to make sure they’re providing the right investments and consulting. Whether you do it in-house or partner with someone that will, compliance with all this is critically important.”

Engaged Mindset

P&C agents are already familiar with the concept of loss control. In the employee benefits space, wellness programs are a similar concept. According to Forrester Research’s Total Economic Impact report, which studied the impact of the Virgin Pulse wellness platform, implementing these programs can reduce business costs related to employee attrition, health care and fatigue-related mistakes.

“Wellness programs are an effective strategy we use to help reduce costs and manage claims,” Engl says. “Lawley has a dedicated team of wellness consultants that work with many employers to develop and implement key wellness strategies that help shape employee behaviors, productivity, and engagement with targeted, thoughtful initiatives and incentives.”

However, employers should be aware that in 2016 the Americans with Disabilities Act was amended in relation to wellness programs. The amendment mandated that employers must “provide reasonable accommodations (adjustments or modifications) that allow employees with disabilities to participate in wellness programs,” according to the Equal Employment and Opportunities Commission (EEOC).

Further, implementing all the right benefits for your insured is only part of the battle. How the program is administered and communicated makes all the difference. More than 4 in 5 employees state that it is very or extremely important to them to be able to manage their benefits online, a sentiment most commonly expressed by millennials, according to the “2022-2023 WorkForces Report” by Aflac. However, the report found that 37% of employers do not offer the ability to enroll in benefits online.

This is another area where a benefits adviser can help employers. “The right technology platform can provide a lot of efficiencies, especially when so many employers are shorthanded,” Engl says. “We can help save them time by streamlining enrollment and managing new hires and terminations, which are also more frequent in 2023.”

Lawley partners with several benefit administration solutions. Finding the right fit depends on the size of the employer, the relationship between the types of benefits they purchase, who the providers are, and the platform they currently use to manage payroll and other operations.

“Each technology platform has its pros and cons depending on what they’re trying to accomplish, which means it’s important we find the right fit,” Engl says. “Whichever technology vendor is selected, we want to make sure that critical factors are considered and they all work well together.”

Additionally, “employee benefits education is important to successful implementation,” Engl adds. “It helps give employees confidence in their benefits package and highlights the value that employers are providing their employees.”

An appealing benefits package consisting of must-haves and tailored solutions will increase employee retention, solving another persistent problem for employers. Replacing an employee can cost up to 150% of their annual salary and even more for C-suite positions, according to Peoplekeep.com.

“A strong benefits package will make an employee think twice before leaving a company,” Belletto says. “Similarly, before a new hire signs a contract with a company, the benefits on offer could be a factor.”

Amidst a wide variety of employee needs, staff spread out across multiple states and a tight labor market, “there’s a big burden being put on companies to do more with less,” Branch says. “They are trying to administer these programs with less people, as well as engage with employees, many of whom are working remotely.”

“Companies want a benefits consultant that is going to go beyond just finding a cheap medical plan,” he adds. “Employers are asking us, ‘What more can you provide for me from a service standpoint beyond the quote? Because I’m trying to do it all and I just can’t.'”

Will Jones is IA editor-in-chief.

This month’s issue

The August issue is out now!