Brick by Brick: Replacement Cost, Commercial Property and the Hard Market

By: Will Jones

“One of my commercial clients called me last month, and it was one of those conversations where he was complaining about the cost of his property coverage going up,” says Matthew Layson, commercial specialist, CalRose Insurance in Everett, Washington. “I was like, ‘Yep, that is a reasonable complaint. I understand why you feel that way.'”

“But then I had to say, ‘And by the way, you’re underinsured. We need to increase the amount of coverage, and you’re actually going to have to pay more,'” Layson recounts.

This conversation is probably familiar to most agents and brokers offering commercial property coverage to clients over the past few years, where the coalescence of multiple interconnected external pressures has created what the American Property Casualty Insurance Association dubbed “the hardest market in a generation.”

Where did it all begin? At the end of the fourth quarter in 2016, MarketScout said, “The soft market is now 16 months old, though it seems longer because the composite rate in 2015 was flat or plus 1% for the first eight months [of 2016] before slipping into negative territory,” noting that “commercial property moderated in December from down 3% to down 2%.”

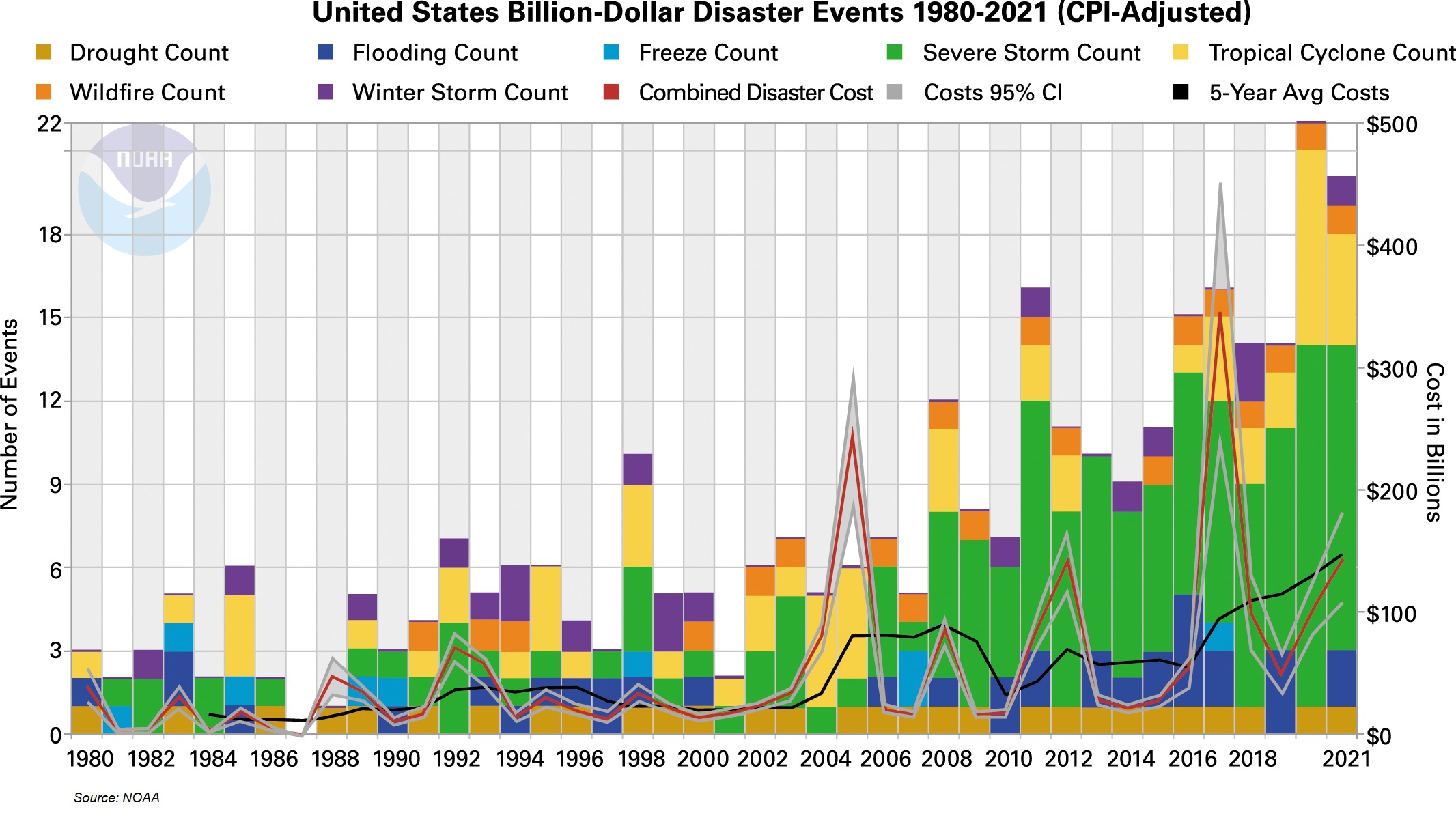

This moderation showed the first signs that the skies were darkening, literally and figuratively, on the market when in September 2016, Hurricane Matthew, the first of a series of devastating storms that would batter the U.S. East Coast, caused more than $4 billion in insured losses, excluding flooding, business interruption or contents claims, according to CoreLogic.

Rate moderation accelerated when the following year’s Atlantic hurricane season was worse, mainly due to a trio of storms—referred to collectively as the HIM Storms (Harvey, Irma and Maria)—which created a combined total of over $200 billion in losses, according to Lloyd’s of London, and each charted in the all-time top-10 costliest natural disasters in American history. Meanwhile, in the Western U.S., 2017 and 2018 consecutively set new records for wildfire destruction, according to the National Oceanic and Atmospheric Administration.

As a result, “the U.S. P&C Insurance Market saw a drastic increase in rates on all lines of coverage,” Assurex Global reported at the end of 2019, highlighting a 5.25% increase in property rates.

In 2020, COVID-19 sent the U.S. economy into a tailspin. In addition to ushering in the worst levels of inflation the U.S. and many of its key trading partners had seen in decades, it wrought supply-chain disruption and labor shortages.

After 2020’s wildfire season set new records once again and the economy buckled under the pressure of the pandemic, the price of lumber skyrocketed and many other materials used for construction followed suit. The combination of inflation, delays and CAT events put immense pressure on insurers making payouts for property losses, which are exacerbated by business income claims and other reimbursements.

Additionally, winter weather, particularly in Southern states, has been a driver of losses. In February 2021, Winter Storm Uri, which primarily hit Texas, resulted in 456,531 insurance claims with an expected total payout of $8.2 billion to insured Texas losses, according to the Texas Department of Insurance.

The following winter, Winter Storm Elliott brough 56 inches of snowfall on Buffalo, New York, and record-low temperatures across the country. Between December 2022 and January 2023, Elliott caused a dramatic 428% increase in freeze claims, according to Verisk, which found the severity of freezing claims had more than doubled compared to 2021, and the cost of replacing drywall, paint and other materials all outstripped national inflation.

A Market in an Economic Storm

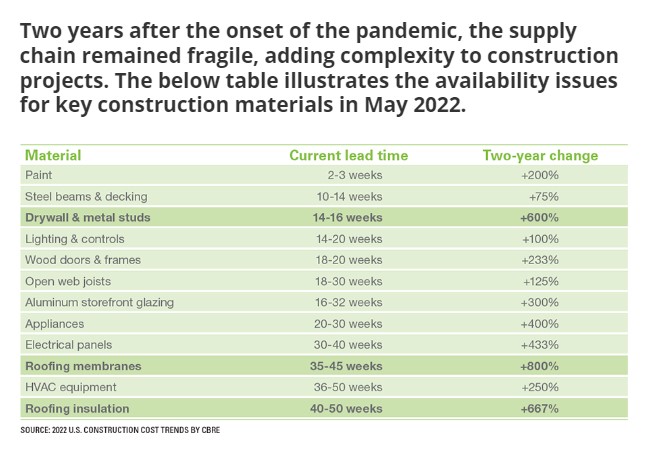

Last year, U.S. construction costs were forecast to increase 14.1% year over year, according to a report from commercial real estate services and investment firm CBRE. The firm noted that the projected increase for 2022 exceeded 2021’s 11.5% rise and “well outpaces” the historical average gain of 2% to 4% per year.

CBRE’s report also highlighted material shortages and longer-than-usual lead times for material delivery, the latter of which increased by 35-45 weeks for roofing materials, according to CBRE. Meanwhile, in construction there was an average of more than 390,000 job openings per month in 2022, according to Associated Builders and Contractors.

As the confluence of catastrophes and inflation caused losses to creep, one more factor has compounded the property market’s troubles: the January 2023 reinsurance renewals, which play a major role in the capacity for the market.

In what was widely considered the most challenging renewal period in 20 years, the cost of property catastrophe reinsurance, which shoulders losses from hurricanes and other natural disasters, increased 45%-100% for loss-hit policies, according to a report published by Gallagher Re.

“The broker put this down to the impact of Hurricane Ian, which struck Florida and South Carolina last year, as well as the threat from inflation, which drives up payouts,” reported the Financial Times. At the end of the second quarter of 2023, the commercial property composite rate stands at 9.5%, according to Market Scout, leaving the market and insureds in dire straits.

“Commercial rates have been rising for three or four years in a row now, and it doesn’t really show signs of abating,” says Victor dos Santos, head of commercial insurance, SageSure. “It might slow down, but I don’t think we’re going to hit negative territory anytime soon. It’s hard to tell whether we’ve even hit the peak.”

The Industry Reacts to Headwinds

The Industry Reacts to Headwinds

“The overall commercial property market is challenged,” says Brian Elliott, senior vice president of Catalytic Risk Managers, a member of the DUAL North America Inc. group of companies, who writes coastal exposed property from Texas to Maine and points out that after Hurricane Ian and in the build-up to the January reinsurance renewals, there was an expectation that “it was going to be painful” and “there was a lot of disorganization because many reinsurance renewals did not get finalized until February.”

This disorganization meant that many companies did not fully understand the cost of capital until the end of the first quarter and were unable to strategize and communicate it effectively until the beginning of the second quarter. “Now it’s really taking hold, and there are certain companies who have made some pretty abrupt moves and have had to cease writing business,” Elliott says.

Most notably, State Farm announced that it will no longer accept new applications for homeowners or commercial property insurance in California. State Farm was the largest homeowners insurer in the U.S. with a market share of 18.35% and more than $24 billion in direct premiums written, according to data from the National Association of Insurance Commissioners.

Two weeks later, Nationwide sent an email to its agents explaining that it is exiting or pausing writing business in multiple states. Affected lines included small commercial and personal lines. In addition to nonrenewing monoline small commercial auto policies starting with late-September effective dates, the company told agents it would pause new writings for small commercial habitational and lessor’s risk countrywide effective June 30.

“Strong headwinds brought on by the economic environment, catastrophic weather events and the impacts of inflation on repair and replacement costs, along with severity and frequency of driving trends, continue to impact the entire insurance industry,” the email said.

Meanwhile, many other carriers have made similar, less public decisions to leave property markets. Most notably, Allstate told the San Francisco Chronicle in June that it exited the California property market last year.

But as companies fled California, a crisis in Florida has been playing out as well. In July, Farmers Insurance said it will stop offering home, auto and umbrella policies in Florida. The move is estimated to affect around 100,000 insureds. The state placed six insurers into receivership in 2022 because of insolvencies, and in February, St. Petersburg-based United Property & Casualty, which wrote about 135,000 policies in Florida, was forced into insolvency after Hurricane Ian.

Compounding the Florida market’s worries in the near term is a tort reform bill signed into law in March that introduced significant changes to how lawsuits are litigated in the state. The new law modified numerous statutes, including changes related to statutes of limitation, comparative negligence and the admissibility of evidence of medical charges at trial.

In the less-than-24-hour period between when the Florida Senate passed the law—in a 23–15 vote—and Governor Ron DeSantis signed it into law, the American Bar Association estimates that more than 100,000 new filings were submitted. With the courts backlogged, insurers are faced with a mountain of costs to defend these claims, which are only expected to damage those carriers’ overall loss ratios and add to national instability.

In the Florida commercial property market specifically, the bill provides some relief by creating a presumption against liability for owners and operators of multifamily residential property in cases based on criminal acts upon the premises by third parties, according to law firm Adams and Reese.

While many companies have now communicated their national strategy for 2023, albeit by the middle of the year, “there’s not a lot of comfort because there’s certain segments in the market that are under-capitalized,” Elliott explains. “The natural results of that lack of supply with constant demand are prices surging in certain areas and a high accumulation of carriers that, historically, have performed poorly.”

Insurers Respond with Tightening Terms

With more companies expected to withdraw from the property markets, the dwindling number of underwriters at companies that continue to write or place business are under increasing pressure. This means that “in today’s environment, agents need to be patient and need to give the underwriting process more time,” dos Santos says.

Another knock-on effect of losses and capacity issues is the inclusion of suboptimal coverages, which means “there are a lot of things that you have to be on the lookout for,” says Coley Boone, CIC at Thames Batré Insurance in Mobile, Alabama.

“Forms can change from special to basic, or the roof goes from replacement cost to actual cash value,” Boone says. “We’re also seeing wind deductibles increasing with minimums. If you have a 5% wind hail deductible, but with a $100,000 minimum, that 5% doesn’t mean that much if you’ve got a $200,000 building.”

Exterior insulation and finish systems (EIFS) exclusions on property are also common. EIFS are multilayered exterior cladding systems designed to provide high energy efficiency in both residential and commercial buildings, such as synthetic stucco, according to the Insurance Risk Management Institute, and were originally excluded from policies due to a high likelihood of capturing water that leads to mold.

Research conducted by the Oak Ridge National Laboratory and the Department of Energy found that EIFS are the “best-performing cladding” in relation to thermal and moisture control when compared to brick, stucco and cementitious fiberboard siding. However, it is significantly more expensive than alternatives.

And as companies count the losses of successive and record-breaking losses in hurricane-prone areas, some use a hurricane minimum earned premium, which refers to the minimum amount of premium that a policyholder must pay, regardless of whether or not a hurricane occurs during the policy period. Often, they are around 75% or 80% of the total policy and without proper advice “that can be very costly to people,” Boone points out.

Similarly, as businesses struggle with the increasing cost of doing business and growing economic anxiety, some are prone to be taken advantage of. “Some direct writers provide quotes without wind and then come in later with the wind quote,” Boone says.

Finding Certainty in Policy Language

“If I had to describe the commercial property market in one word, I’d say ‘volatile,'” says Josh Gurley, President of HM Advisors in Warner Robins, Georgia. “Between reinsurance cost, inflation and increased cost of construction, the landscape is constantly changing.”

The unpredictable costs of construction mean that determining an accurate replacement cost for a commercial property is bordering on impossible. Typically, agents use replacement cost estimators to determine how to insure a property. However, the volatility means that they can be “inaccurate,” Gurley explains.

“Some of the replacement cost estimators are still a little bit behind inflation because the prices of commodities change every single day and, as agents, we have to be very nimble in our valuations,” he says. “Commodities are traded in real-time, and the price can change on a dime—ask anybody that’s built a building in the past couple of years.”

“Asking how much it costs to replace something is kind of like asking, ‘How far is it from here to over yonder?'” Gurley adds. “We don’t really know exactly.”

In an ideal world, Gurley is presented with a newly constructed building and is offered to quote the replacement cost based on the build sheet for the building. In that instance, “we can see the exact cost per square foot and compare it to other buildings we’ve insured,” he says.

However, determining replacement cost in the current commercial property market is a far from ideal scenario. Still, agents can show their value by providing insight into coverages. “On any account where it’s eligible, we try to write everything on a blanket limit, and we have 100% coinsurance,” Gurley says.

Blanket limits can apply to all types of property at one business-owned location or similar types of property at many locations, according to Investopedia. The major advantage of purchasing this type of policy is that the entire coverage limit applies to one property if it is significantly damaged or destroyed.

“Agreed amount and no margin clause is another big thing that we try to add to these policies,” Gurley says. “We request all forms and try to negotiate what we need up front.”

A margin clause is a nonstandard commercial property insurance provision stating that the most the insured can collect for a loss at a given location is a specified percentage of the values reported for that location on the insured’s statement of values, according to IRMI, while agreed amount suspends coinsurance.

Further, “more than ever, insurers want best-in-class risk,” Gurley says. “Everybody should be reviewing their protective safeguards. Building owners should enforce no smoking and have well-maintained sprinklers and dust collection systems.”

For example, the Florida tort reform passed in March that creates a presumption against liability for owners and operators of multifamily residential property only “applies to such owners who implement certain security features, including but not limited to lighting in common areas, a one-inch deadbolt in each dwelling unit door, window locks, and gates around pool areas,” according to law firm Adams and Reese.

“There’s a lot of things that insurers are looking for, and they are being sticklers,” Gurley adds, noting that in industrial environments, businesses can protect the building by ensuring certain types of metals are not mixed, which can lead to explosions; paint booths are NFPA compliant; employees wear respirators; the air is clean; and other safety practices are followed.

Data has always been the fulcrum of the insurance industry. However, when determining replacement cost, even the numbers can lie based on what estimator an agent is using, which means “you have to be astute,” Layson says. He points out that his agency uses different estimators—one from a third party, as well as a carrier estimator—on the same property to find an accurate amount.

Piecing Together Accurate Replacement Cost

“With building values jumping up so much in the past three years, it’s really hard to know what to trust,” Layson says. “If you’re using at least two different data points, and they both say it’s going to cost $1.2 million to replace a building, you can feel pretty confident.” Again, in an ideal world, the estimators will match, but “sometimes, there can be pretty massive variations, such as a 20% swing,” he says.

And as economic anxiety increases and the hard market pushes premiums higher, 51% of consumers said they are looking for ways to save money on their existing insurance policies, according to a recent Agency Forward study from Nationwide. When asked how they are saving money on insurance, 26% are decreasing or plan to decrease coverage or limits on existing policies, 23% have or are considering switching to a new insurance agent, and 20% have already removed a policy from their coverage or plan to in the next six months.

This price sensitivity means that property owners may be more inclined to list a lower replacement cost than what an estimator suggests, or the pre-inflation amount, to save money on their premium. “Occasionally, I do have to push my client a little bit and say, ‘Hey, that’s way too low’ or ‘the company won’t go that low’ because they’re not thinking about the claim in the future,” Layson says.

If a property owner’s fixation on price may not be in their best interests, it presents another opportunity for agents to position themselves as the expert.

“It’s a bit of a dark horse, and I’m sure a lot of agents will hate me for even saying this, but one conversation I have is about moving from replacement cost to actual cash value,” Layson says. “If my client’s going to take 30 minutes of my time to complain about price, then we’re going to take another 30 minutes where I’m going to give them options—even if they’re bad ones.”

“I say, ‘OK, here is an option, this is how it’s going to function, and this is what would happen if things went bad,'” Layson explains. “When I have those coverage reduction conversations because people are frustrated with price, nine times out of 10 they arrive at the conclusion that they shouldn’t be doing that.”

And depending on how that conversation goes, a property owner may be inclined to add a 25%-50% extended replacement cost endorsement, Layson explains, which is another solution that can be used to ensure the replacement cost is accurate amidst inflation. However, it is more commonly used in personal lines and difficult to find in commercial property.

The Art and Science of Industry Relationships

If working with a price-sensitive clientele and cautious underwriters to determine a replacement cost estimate that is both adequate and affordable is an art, the data behind that number is most definitely a science.

Whether an estimator is provided by a carrier or another third party, “it’s important that agents interview the providers right back in terms of their basis for producing replacement costs,” says Doug Brekke, vice president of underwriting and product, SageSure. “What’s the factual basis? How confident are they in it? Are they using a broad-brush approach? Or do they have granular data?”

Naturally, the type of construction materials used in a building can impact the cost of insurance coverage. Buildings constructed with high-end or specialized materials typically have higher replacement costs compared to those built with more common or standard materials. Additionally, buildings utilizing fire-resistant or impact-resistant materials, such as steel roofs, may have higher upfront construction costs but could result in lower replacement costs in case of damage.

Additionally, the size and shape of the structure affect the amount of materials required for construction, and complex or intricate designs often involve specialized construction techniques and materials that may be costlier to replicate in case of damage or destruction. Unique architectural elements or historical preservation requirements can also contribute to high replacement costs.

For these reasons, it is crucial for agents and brokers to provide as much information as possible about a building to the underwriter. Doing so can benefit the client, agent and insurer with more accurate underwriting and pricing, and faster turnaround time.

“A lot of information is publicly available and research on the front end can be the difference between a few hours versus a few days for an agent to obtain a quote,” Brekke says, adding that that “inaccurate or missing information can lead to underinsured policyholders and premium leakage. Spending a little more time doing diligence on the front end actually is additive on the back end for the agency’s economics.”

“When the replacement cost is ridiculously low, we don’t want to spend time on it, because we don’t want to go on this long tiresome Easter egg hunt for information,” Elliott agrees. “We can turn things around really quickly when you take as much inefficiency as you can out of the process—and the best way to do that is to provide as much information as possible.”

“One of the most important things that you can do, especially in this market, is have a great submission,” Gurley adds. “A great submission is going to include a full narrative, a diagram, all the claims, history, ACORD applications and everything that the underwriter’s going to need to get your submission to the top of the stack.”

Being kind to your underwriter by giving them the information can be taken a step further by being as committed to the relationship with your company partners as you are to your clients.

“If you’ve got a good connection with your carrier and your underwriter, they’ll give you heads up about things coming down the pipeline, like changes in appetite,” Layson says, “which can make remarketing an account that little bit more seamless.”

“Agents that pay attention to their carriers and don’t just view them purely as a product line get an advantage,” Layson adds. “That way, it’s not a shotgun wedding. It’s just a, ‘Hey, the other carrier’s not offering that anymore, and so we’re moving you over here.'”

And with premiums continuing to rise, constant communication with clients is crucial, Boone explains. She tries to touch base with clients every six months at a minimum. “There’s nothing worse to me than delivering a substantial increase within days of an expiration date,” she says. “Then you feel like you’re handcuffing your insured because they don’t have time to do anything else.”

While the hard market, inflation and a stagnating economy provide various business challenges, not least for insuring property, “it gives us an opportunity to show our value, provide good sound advice and build loyalty,” Boone adds. “If we can build a book of business, call out the commodity buyers and further our relationships during a hard time, we’re going to be golden.”

Will Jones is IA editor-in-chief.

This month’s issue

The July issue is out now!