Trump Accounts: What You Need to Know About the New Individual Saving Vehicle

By Christine Muñoz

Among the many provisions tucked into the recently passed One Big Beautiful Bill Act is the introduction of yet another savings vehicle: the Trump Account. This new type of individual retirement account adds to the growing list of options for families looking to plan ahead financially.

The total U.S. fertility rate—the average number of children a woman is expected to have over her lifetime—has dropped to 1.6, according to the Centers for Disease Control and Prevention, well below the 2.1 needed to maintain a stable population.

One contributing factor is the high cost of raising a child. The average cost to raise a child in the U.S. through age 17 is about $310,000, according to a 2022 Brookings Institution study. That number can be significantly higher depending on location and lifestyle.

The Trump Account is designed to ease some of that burden while encouraging long-term savings for children.

More on Employee Benefits

How the Trump Account Works

Here are the key features:

- Eligibility: Children born between 2025 and 2028.

- Initial government contribution: A one-time $1,000 deposit from the federal government.

- Annual contributions: Parents, relatives and others can contribute up to $5,000 annually, post-tax.

- Employer contributions: Employers may contribute up to $2,500 per year, adjusted for inflation starting in 2027. These contributions are excluded from both the employer’s and employee’s taxable income and count toward the $5,000 total limit.

- Access: Funds may be withdrawn by the child starting at age 18.

- Investment options: Funds must be invested in a qualified mutual fund—specifically, one that tracks the S&P 500 or another index focused primarily on U.S. equities.

As with all tax-advantaged accounts, there’s fine print, especially around investment eligibility and qualifying criteria for children.

For independent insurance agencies, this could be an innovative, family-focused benefit to offer employees. While the maximum employer contribution is $2,500, companies could choose to offer smaller amounts. The benefit is flexible, tax-advantaged and aligns with long-term financial wellness goals.

Agency Group Benefits Made Easy

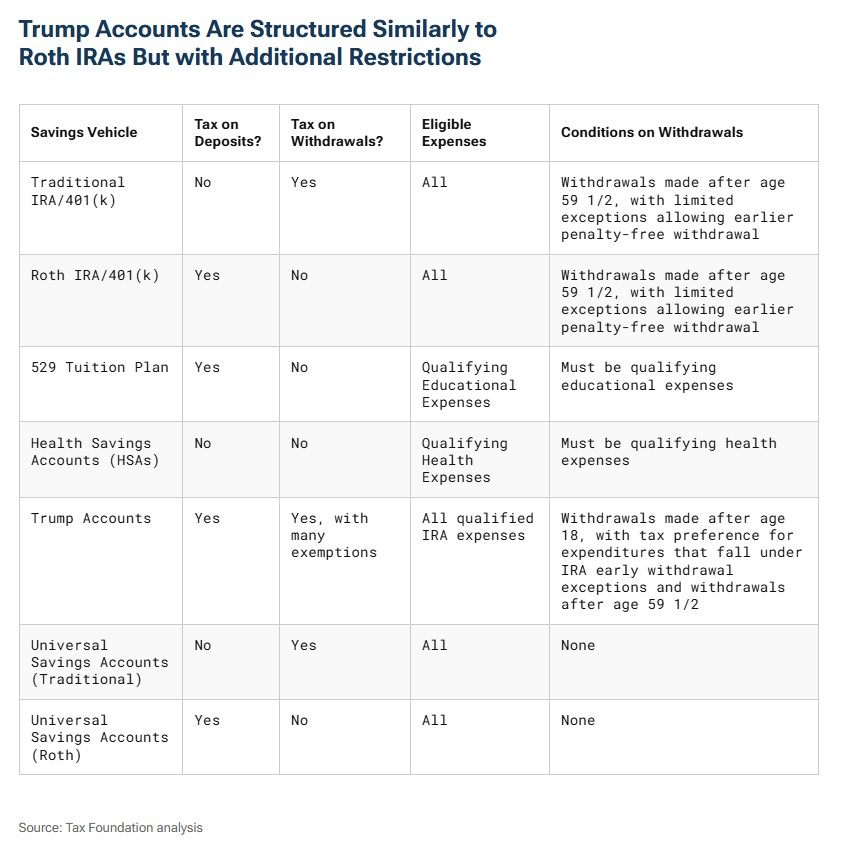

How Does the Trump Account Compare to Other Retirement Vehicles?

Depending on the individual’s goals, income and timeline, it may make sense to prioritize contributions to a traditional individual retirement account (IRA), Roth IRA, 529 tuition savings plan, Trump Account or another retirement vehicle.

The Tax Foundation published a chart that outlines the features and benefits of each type of account:

Independent agents and brokers are uniquely positioned to guide both families and business clients through the growing maze of savings and benefits options. Whether it’s helping employers add innovative tools like the Trump Account to their benefits package or advising personal lines clients on long-term financial planning, these conversations strengthen relationships and demonstrate the value of trusted advisors.

Christine Muñoz is Big “I” assistant vice president of retirement and benefits. Big “I” Employee Benefits and Big “I” Retirement offers varying lines of coverage to meet the diverse needs of Big “I” members. For assistance setting up retirement savings vehicles, contact Muñoz or visit Big “I” Employee Benefits and Big “I” Retirement.

Agency Management Solutions

Insurance Markets

Big I Programs

This month’s issue

The March issue is out now!