Public Insurance Broker Performance Trends and the Impact on M&A

By Mark Crites

The performance of publicly traded insurance brokers offers real-time insight into how investors view our industry. There are only nine of these firms; five longstanding public brokers—AON, Brown & Brown, Gallagher, Marsh and Willis—and four newer publicly traded firms—Baldwin, Goosehead, Ryan and The Woodlands Financial Group.

Reagan Consulting actively monitors stock price changes for this group throughout the year. 2025 has told a tale of two very different market realities for public brokers.

Public broker stock prices have been on an absolute tear over the last decade, and the first quarter of 2025 started on the same foot. Public brokers were up 15% through March compared to the S&P 500, which was down 4% during the same period. However, the second and third quarters of 2025 were different stories. Since March, public broker stock prices have fallen significantly. At one point, they were down 9.2% for the year. As of Oct. 10, the S&P was up 11.4%.

make Your Voice heard at the 2026 Big ‘I’ Legislative Conference

April 22-24 Washington D.c.

Investors have been enamored with the insurance brokerage industry for years. So, what changed? The slowdown in organic growth, and more specifically, the impact of softening property & casualty pricing.

Public brokers, excluding Goosehead, posted an average organic growth of 6.7% in the second quarter of 2025 versus 9.4% in the second quarter of 2024. The median change in growth for public brokers was-4% in just 12 months.

Privately held brokers did not experience the same abrupt drop in growth in the second quarter of 2025, as measured by Reagan Consulting’s “Growth & Profitability Survey.” But what’s caused the difference in growth profiles?

It could be a combination of two things. The first is accounting policies. Public brokers adopted ASC 606, which accelerates the impact of rate changes. The second is the business mix. Larger accounts have been hit with softer rates, along with more professional lines exposure.

Even with organic growth levels over historical norms, a decelerating growth picture led to stock prices to fall for almost all public brokers after the second quarter earnings were released.

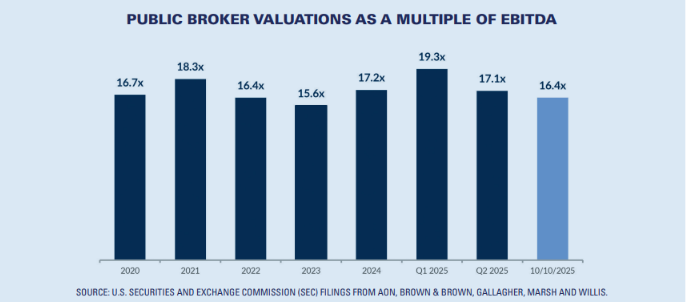

Public broker valuations peaked at the end of the first quarter of 2025 at 19.3x LTM EBITDA (last 12 months earnings before interest, taxes, depreciation and amortization), following a blistering start to the year.

Then, with lower organic growth results than anticipated, second-quarter valuations dropped by over 2x LTM EBITDA in just three months. This represented one of the sharpest changes ever recorded quarter over quarter.

Third-quarter earnings have yet to be released for any firm. Still, valuations through September show that public broker multiples have come down even further to 16.4x LTM EBITDA, the lowest level since 2023.

But what impact, if any, does this valuation change have on M&A activity? While the fall seems drastic, multiples still remain at historically high levels. These valuations may apply a little pressure to the private markets, which generally operate at a slight discount on the public markets.

That being said, there are no signs from either public or private buyers of a reduced appetite for acquisitions. Reagan Consulting expects overall broker merger & acquisition (M&A) activity to remain consistent with 2023 and 2024 levels—but perhaps with more selectivity from buyers seeking to improve organic growth in a softening market.

Mark Crites is a partner at Reagan Consulting.

News Types

Agency Management Solutions

This month’s issue

The February issue is out now!