Broker Led M&A Deal Flurry Set to Continue in 2022

By: Mike Bendokaitis

Mergers & acquisitions activity in the insurance brokerage space is occurring at a record-setting pace and there are no signs of a slowdown in 2022. Brokers backed by private equity (PE) are displaying aggressive acquisition strategies in buying up independent agencies, and record valuations are prompting agency owners to sell.

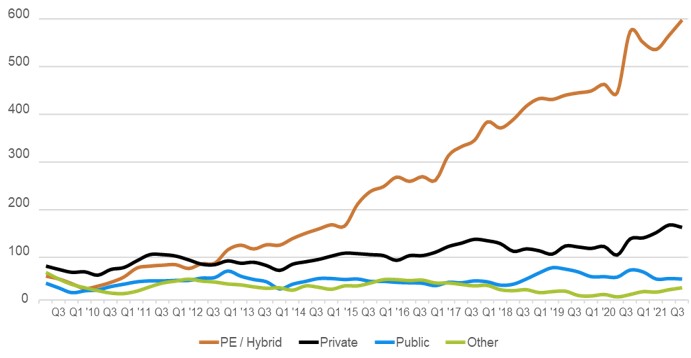

Through the third quarter of 2021, there were an estimated 550 deals, an increase of approximately 12% over the same period in 2020, according to data pulled from S&P Capital IQ. Year-end figures are not yet available, but we can expect to see more than 300 deals closed in the fourth quarter of 2021, surpassing last year’s fourth-quarter total of 290.

Armed with large cash reserves, PE-backed brokers deployed capital at a record pace and accounted for about 70% of deal activity through the third quarter of 2021, according to OPTIS Partners. At the same time, privately owned agencies and brokers are leveraging the low cost of capital to execute growth plans via M&A.

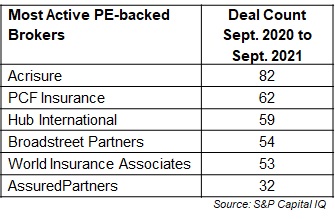

Established broker Acrisure led the way in announcing 82 acquisitions over a 12-month period from September 2020 to September 2021. Newer entrants, such as PCF, are beginning to make their mark with 62 acquisitions over the same period. Privately owned agencies and brokers represented 20% of all deal activity within the space, a year-over-year increase of 17%.

Record valuations and the looming threat of a sizable increase to capital gains tax have been among the primary factors leading agency owners to sell. Increased competition and overall growth of the industry pushed deal multiples as high as 10.5 times earnings before interest, taxes, depreciation and amortization (EBITDA) in 2021. This is a notable increase over prior years and will be a factor to watch in 2022.

2022 Outlook

Several notable tailwinds should carry over into 2022 and drive significant M&A activity in the brokerage space.

Despite ongoing consolidation, the industry remains heavily fragmented. There are about 36,000 independent property and casualty insurance agencies in the U.S., according to the Future One 2020 Agency Universe Study. Despite the high volume of acquisitions between 2018 and 2020, this number remains roughly flat driven in part by the deterioration of the captive agency channel and the low barriers to entry of starting an independent agency.

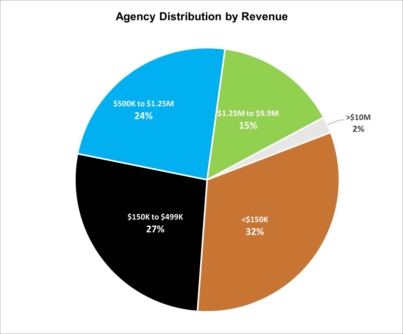

A vast majority of agencies are relatively small, with 83% of agencies realizing less than $1.25 million in annual revenue according to the Insurance Information Institute. At this scale, agencies have limited negotiating power with carriers and back-office capabilities. Consolidation of agencies within this segment or acquisition by larger brokerages benefit involved parties through economies of scale, enabling increased negotiation power for commissions and a wider breadth of products and services.

A vast majority of agencies are relatively small, with 83% of agencies realizing less than $1.25 million in annual revenue according to the Insurance Information Institute. At this scale, agencies have limited negotiating power with carriers and back-office capabilities. Consolidation of agencies within this segment or acquisition by larger brokerages benefit involved parties through economies of scale, enabling increased negotiation power for commissions and a wider breadth of products and services.

The positive industry outlook and fragmentation make this sector increasingly attractive to investors and, as a result, we expect to see increased investments from existing firms and new players entering the market.

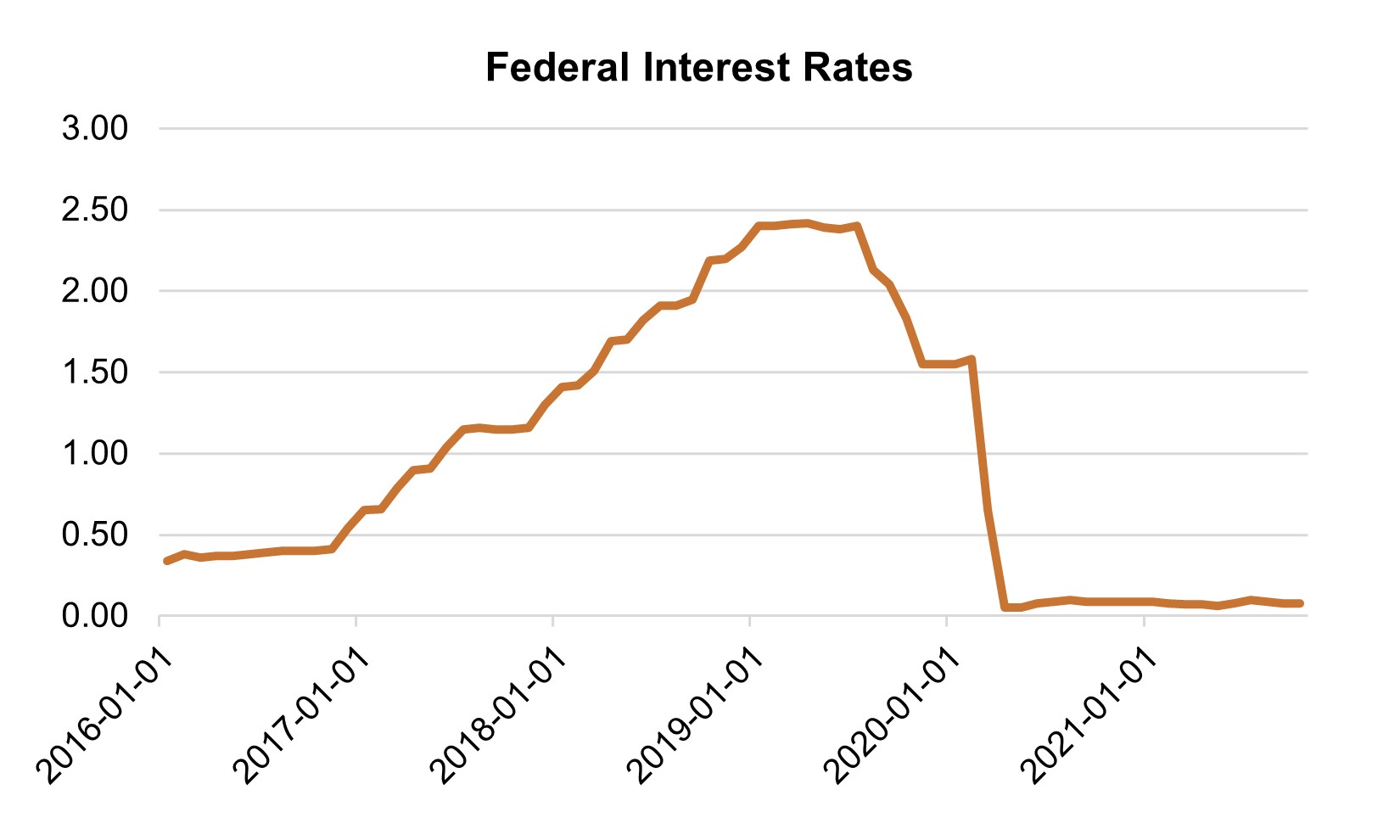

Additionally, persistently low interest rates will continue to be a tailwind, enticing financial sponsors to significantly expand their footprints. Investors have accomplished this through aggressive borrowing and adding leverage to the balance sheets of their portfolio companies. The Federal Reserve indicated that it may begin to moderately raise interest rates in the third quarter of 2022, which could slow M&A activity in the latter part of 2022. However, the potential threat of higher rates may simply accelerate activity during the first part of the year.

Increasing competition will drive product diversity and brokers will look to supplement growth by acquiring specialty lines and ancillary services. Emerging lines such as cyber, cannabis and consumer-data privacy provide significant growth opportunities. Subject matter expertise and underwriting capabilities for these lines are scarce throughout the industry. As a result, we expect brokers to turn to M&A to build platforms around these specialty lines to take advantage of this growth opportunity.

Increasing competition will drive product diversity and brokers will look to supplement growth by acquiring specialty lines and ancillary services. Emerging lines such as cyber, cannabis and consumer-data privacy provide significant growth opportunities. Subject matter expertise and underwriting capabilities for these lines are scarce throughout the industry. As a result, we expect brokers to turn to M&A to build platforms around these specialty lines to take advantage of this growth opportunity.

Mike Bendokaitis is vice president of Copper Run, an M&A advisory firm based in Columbus, Ohio.